|

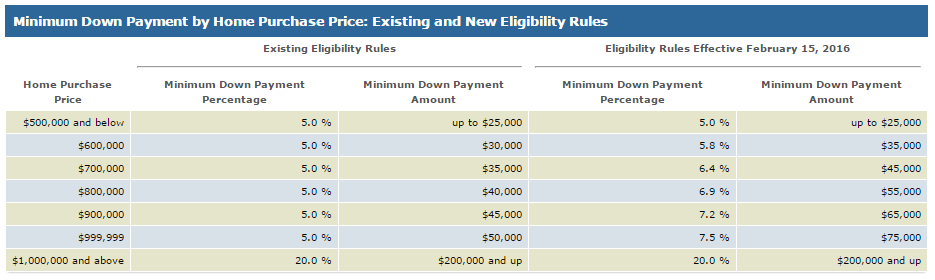

Changes to down payment requirements coming February 15, 2016 Today Finance Minister Bill Morneau announced changes to down payment requirements. Effective February 15, 2016, the minimum down payment for new insured mortgages will increase from five per cent to 10 per cent for the portion of the house price above $500,000. The five per cent minimum down payment for properties up to $500,000 remains unchanged. Homes priced at more than $1 million by law require a minimum down payment of 20 per cent. Today's announcement therefore focuses on homes priced between $500,000 and $1 million. In the Mortgage Professionals Canada (MPC) Fall Report, Chief Economist, Will Dunning discusses why raising the down payment could cause problems for the housing market, including this cautionary observation: “Rising prices have made it increasingly difficult for first-time home buyers to accumulate down payments. Increasing down payment requirements would, most likely, severely dampen housing demands from people who are financially well-qualified to make their monthly mortgage payments.” MPC notes that the 10% requirement does represent a graduated approach while the Ministry of Finance commented that they believe this will only impact 1% of home purchasers. Click here for the government’s official news release. Handy chart below - click to enlarge.

1 Comment

Cash back mortgages used to be about purchasing without 5% down payment. Today you still need to have saved the 5% down payment from your own funds for the purchase. There are cashback mortgages being offered today the incentive being so you can turn around and apply the cash back portion directly on the mortgage for a better effective rate, purchase new furniture, new appliances, or do some renovations on the new purchase.

The catch to the cash back mortgage is if you decide to break it midterm, which most people shouldn’t rule out because you may decide to sell, refinance, or something you just didn’t plan for changes in your life. The fine print is that you not only have to pay the interest penalty, you have to return the cash back portion to the bank. I can work with you to see what options will work best for your situation sometimes the cash back might be the good option but there are other options like the purchase plus improvements or line of credits. If you are thinking of the cash back mortgage give me a call and we can work together to find the best option for you. With some lenders moving towards collateral charge mortgages, it’s important to understand the differences between a collateral and a standard charge mortgage.

The primary difference is that a collateral charge mortgage registers the mortgage for more money than you require at closing. For instance, up to 125% of the value of the home at closing with some banks or 100% through many credit unions, instead of the amount you need to close your transaction (as is the case with a standard charge mortgage). The major downside to a collateral mortgage becomes evident at your mortgage renewal date. For borrowers who want to keep their options open at maturity and have negotiating power with their lender, this isn’t the best product feature because collateral charge mortgages are difficult to transfer from one lender to another. In other words, if you want to change lenders in order to seek a better product or rate in the future, you have to start from the beginning and pay new legal fees, which range from $500 to $1,000. With a standard charge mortgage, in most cases, the new lender will cover the charges under a “straight switch” in order to earn your business. In addition, with a collateral charge, it could be difficult to obtain a second mortgage or a home equity line of credit (HELOC) unless your home significantly appreciates in value. Lenders offering collateral charge mortgages promote the benefit that it makes it easier and more cost effective to tap into your equity for such things as debt consolidation, renovations or property investment. There’s no need to visit a lawyer and pay legal fees – the money is available as your mortgage is paid down. Yet, if you read the fine print, you may still have to re-qualify at renewal. A standard charge mortgage gives you the ability to move to another lender at renewal should you want to without incurring legal fees, and many borrowers find it more beneficial to keep their options open. If you need to borrow more with a standard charge mortgage, you have the option of a second mortgage or a HELOC, which also enables you to take money out as your mortgage is paid down. Navigating through the mortgage process alone can be tricky. Working with a mortgage professional who has access to multiple lenders will help ensure you receive the product and rate catered to your specific needs. Read about how a collateral mortgage can trap you Read about a real life story of the pitfalls of a collateral mortgage CMHC to Increase Mortgage Insurance Premiums

OTTAWA, April 2, 2015 -- As a result of its annual review of its insurance products and capital requirements, CMHC is increasing its homeowner mortgage loan insurance premiums for homebuyers with less than a 10% down payment. Effective June 1, 2015, the mortgage loan insurance premiums for homebuyers with less than a 10% down payment will increase by approximately 15%. For the average Canadian homebuyer who has less than a 10% down payment, the higher premium will result in an increase of approximately $5 to their monthly mortgage payment. This is not expected to have a material impact on housing markets. http://www.cmhc-schl.gc.ca/en/corp/nero/nere/2015/2015-04-02-1605.cfm An important piece of information about home purchasing ... Fill out one box on your tax forms and get a $750 tax rebate!!

The Economic Action Plan includes a First-Time Home Buyers’ Tax Credit (HBTC) to help? The HBTC assists first-time home buyers with the costs associated with the purchase of a home, such as legal fees, disbursements and land transfer taxes, which are a particular burden for first-time home buyers, who must also save for a down payment. When doing your taxes for 2014, check to see if the following criteria apply to you and make sure to make use of this credit: You can claim an amount of $5,000 for the purchase of a qualifying home acquired in 2014, if both of the following apply: -you or your spouse or common-law partner acquired a qualifying home; and -you did not live in another home owned by you or your spouse or common-law partner in the year of acquisition or in any of the four preceding years (first-time home buyer). This means that essentially you can decrease your declared income by $5,000 allowing for reduction in the amount of taxes you owe. The Home Buyers' Tax Credit, at current taxation rates (15%), works out to a rebate of $750 for all first-time buyers. After you buy your first home, the credit must be claimed within the year of purchase and it is non-refundable. |

AuthorRita & Rachel

Archives

October 2023

Categories |

RSS Feed

RSS Feed